Quick verdict

EtherFi Cash is worth considering if you already hold crypto and want a card that lets you spend in the real world without immediately selling assets.

It is not a normal cashback card. The useful part is the crypto-backed account model: card spending, stablecoin rewards, Apple Pay / Google Pay, and the option to borrow against supported assets. The risk is also in that same model: collateral, repayment, exclusions, and regional terms matter.

If you decide to try it after reading the terms, use the special signup link before creating the account so any active extra cashback or referral benefit is attached. Terms and eligibility can change.

Short answers first:

| Question | Short answer |

|---|---|

| Is EtherFi Cash worth it? | Yes, if you already use crypto and understand the credit/collateral rules. |

| How does EtherFi Cash work? | It connects card spending to an EtherFi account instead of acting like a simple prepaid crypto card. |

| What is the cashback limit? | The advertised rate depends on membership level, qualifying spend, and monthly thresholds. |

| What fees should I check? | FX, bank transfers, wires, withdrawals, cash advances, and repayment terms. |

| If you are… | My take |

|---|---|

| Already using EtherFi or DeFi | Worth testing |

| Looking for simple cashback only | Compare against normal cards first |

| Planning to borrow against volatile assets | Read repayment and liquidation rules first |

| Outside supported regions | Check availability before you care about rewards |

How does the EtherFi Cash card work?

Most crypto cards are prepaid cards with a crypto wrapper. You top up, sell, or convert crypto, then spend through a normal card rail.

EtherFi Cash is more interesting because it is positioned as a DeFi-native credit card tied to your EtherFi account. The point is not only “spend crypto.” The point is to keep assets in the crypto account layer while still paying for normal things.

That is why this review focuses less on the card design and more on how the account works: spending, collateral, rewards, limits, and the app experience.

The card is the visible part. The account mechanics are the part that decides whether it is actually useful.

The product positioning is closer to a crypto neobank than a simple prepaid crypto card.

The simple version:

| Card type | How it usually works | Main tradeoff |

|---|---|---|

| Prepaid crypto card | Convert or top up first, then spend | Simple, but less crypto-native |

| Exchange card | Spend from an exchange balance | Convenient, but custodial |

| EtherFi Cash | Spend through a crypto-backed account | More flexible, but terms and collateral risk matter |

Best for / not for

| Best for | Not for |

|---|---|

| Crypto-native users | People who want a normal bank debit card |

| Users who want Apple Pay / Google Pay | Users who dislike collateralized borrowing |

| People spending in USD or EUR | People trying to manufacture cashback |

| EtherFi ecosystem users | Anyone who has not read the card terms |

If you already hold ETH, BTC, stablecoins, or EtherFi assets, the product can make sense because it gives you another option besides selling. If you do not want credit, collateral, or DeFi account mechanics involved in everyday spending, this is probably more complex than you need.

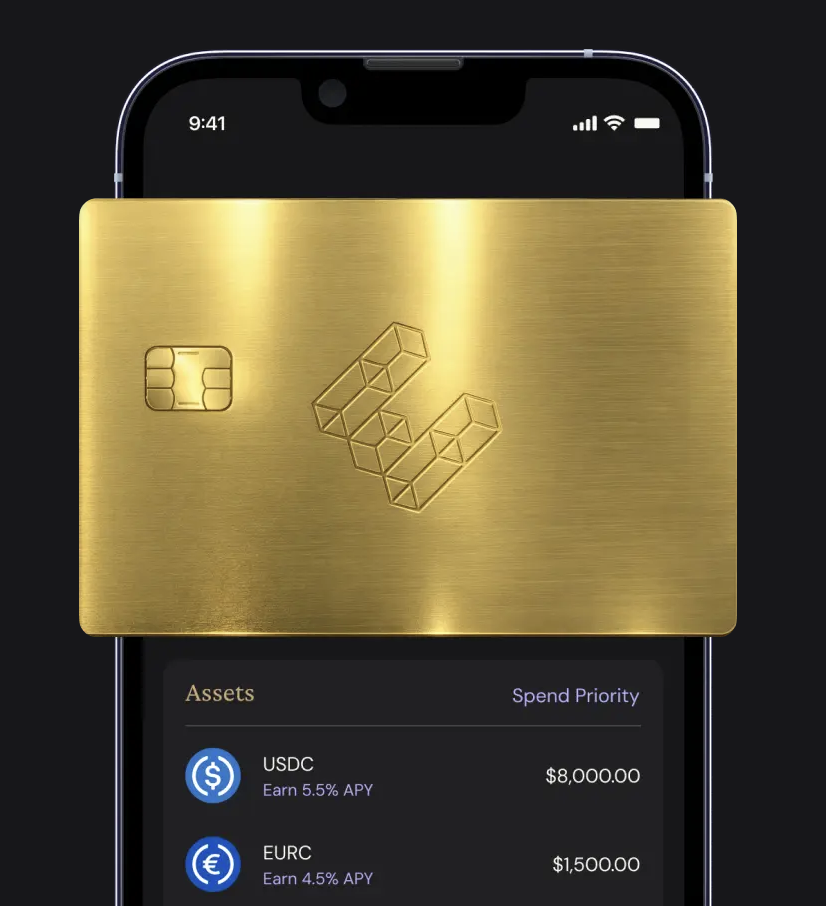

The interesting product detail is the connection between card spending and crypto account balances.

The value in one minute

Here is the short version of what matters:

- Up to 3% cashback on qualifying purchases.

- Cashback is credited as USDC.

- Apple Pay and Google Pay support.

- Virtual and physical card options.

- USD and EUR account support.

- EtherFi advertises 0% FX fees for USD and EUR transactions.

- The account model is positioned around non-custodial crypto infrastructure.

If those tradeoffs fit how you already spend, the cleanest path is to open the card flow through the special link, then verify the current cashback offer inside EtherFi before you finish signup.

The strongest pitch is not only rewards. It is the combination of saving, earning, and spending in one crypto-native account.

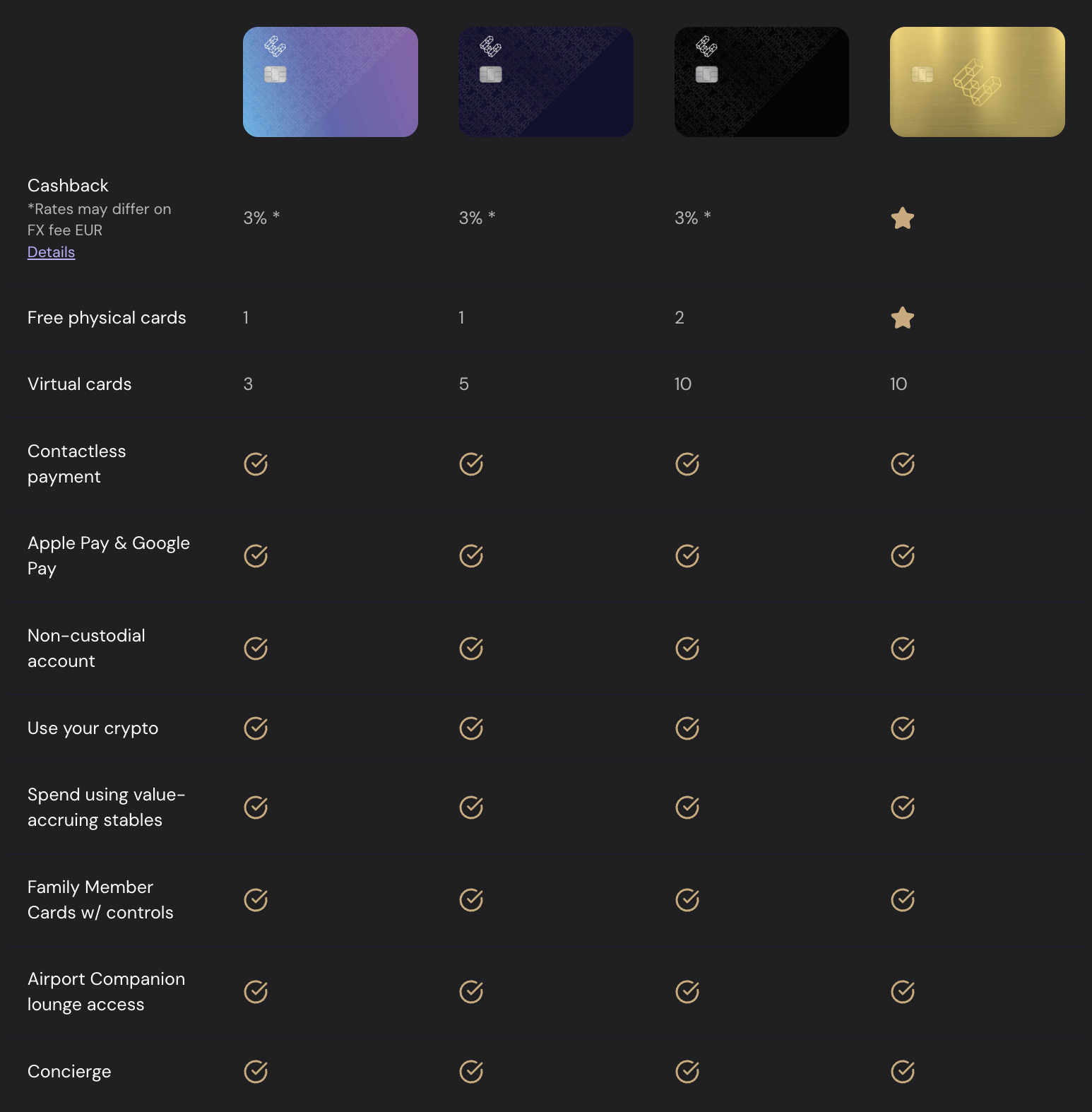

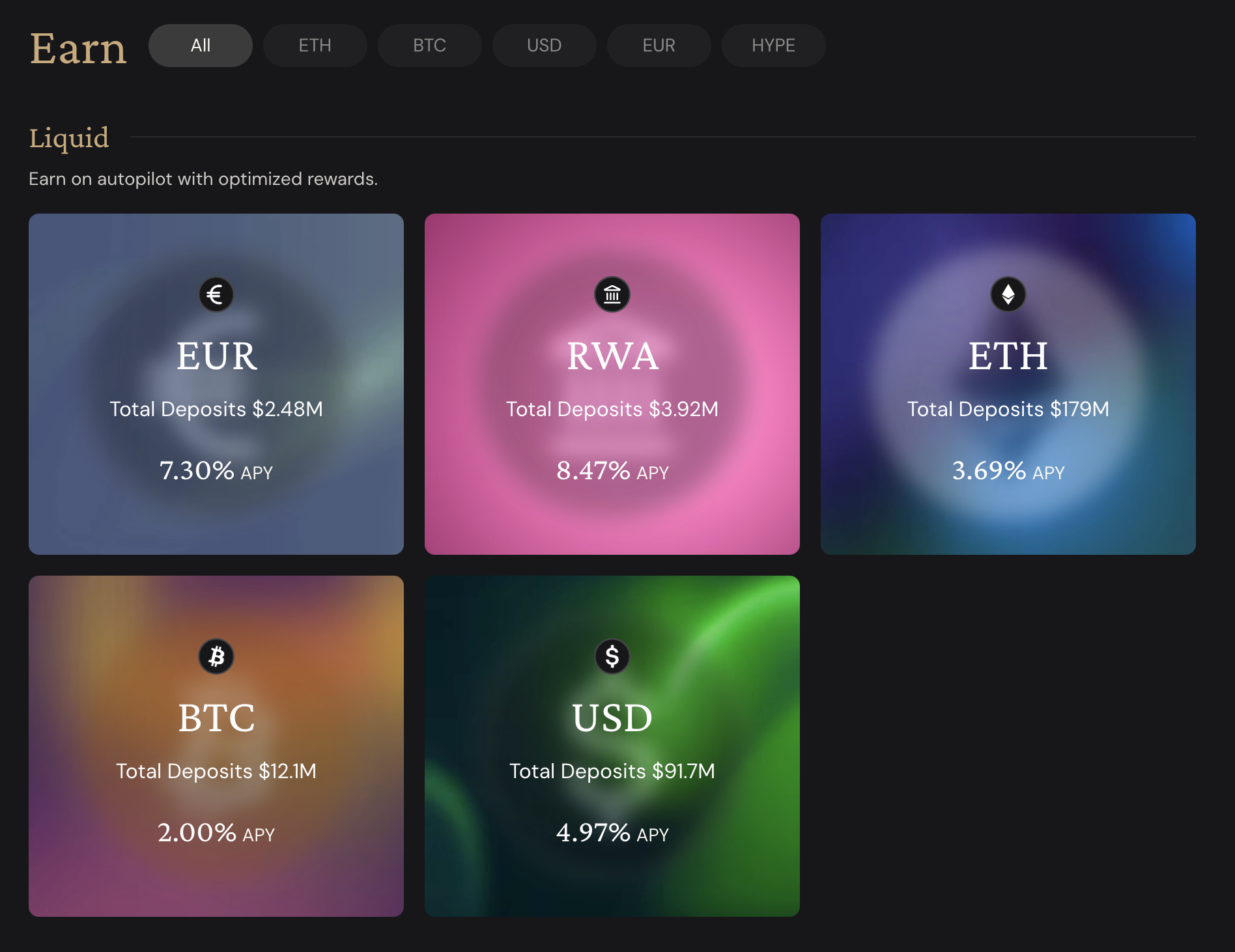

EtherFi cashback limit: what actually matters

The headline is up to 3% cashback. That is useful, but the limit and exclusions matter more than the headline.

For Core members, EtherFi’s help center lists 3% on the first $2,000 of qualifying monthly USD spend, then lower rates after that. Luxe and Pinnacle have higher monthly thresholds before the rate steps down. EUR purchases have their own adjusted ladder because EtherFi also advertises 0% FX on EUR transactions.

The cashback headline depends on membership level, spend threshold, and qualifying purchase rules.

| Spend type | What to know |

|---|---|

| Normal merchant purchases | May qualify for cashback |

| ATM withdrawals | Usually excluded |

| Cash advances | Usually excluded |

| Gift cards and money orders | Usually excluded |

| Refunds | Can reverse cashback |

| High monthly spend | Rate may step down by tier |

The best use case is normal merchant spend: groceries, travel, hotels, restaurants, subscriptions, and business expenses. It is not a card for manufactured spend, cash-equivalent transactions, or trying to force every purchase into a rewards category.

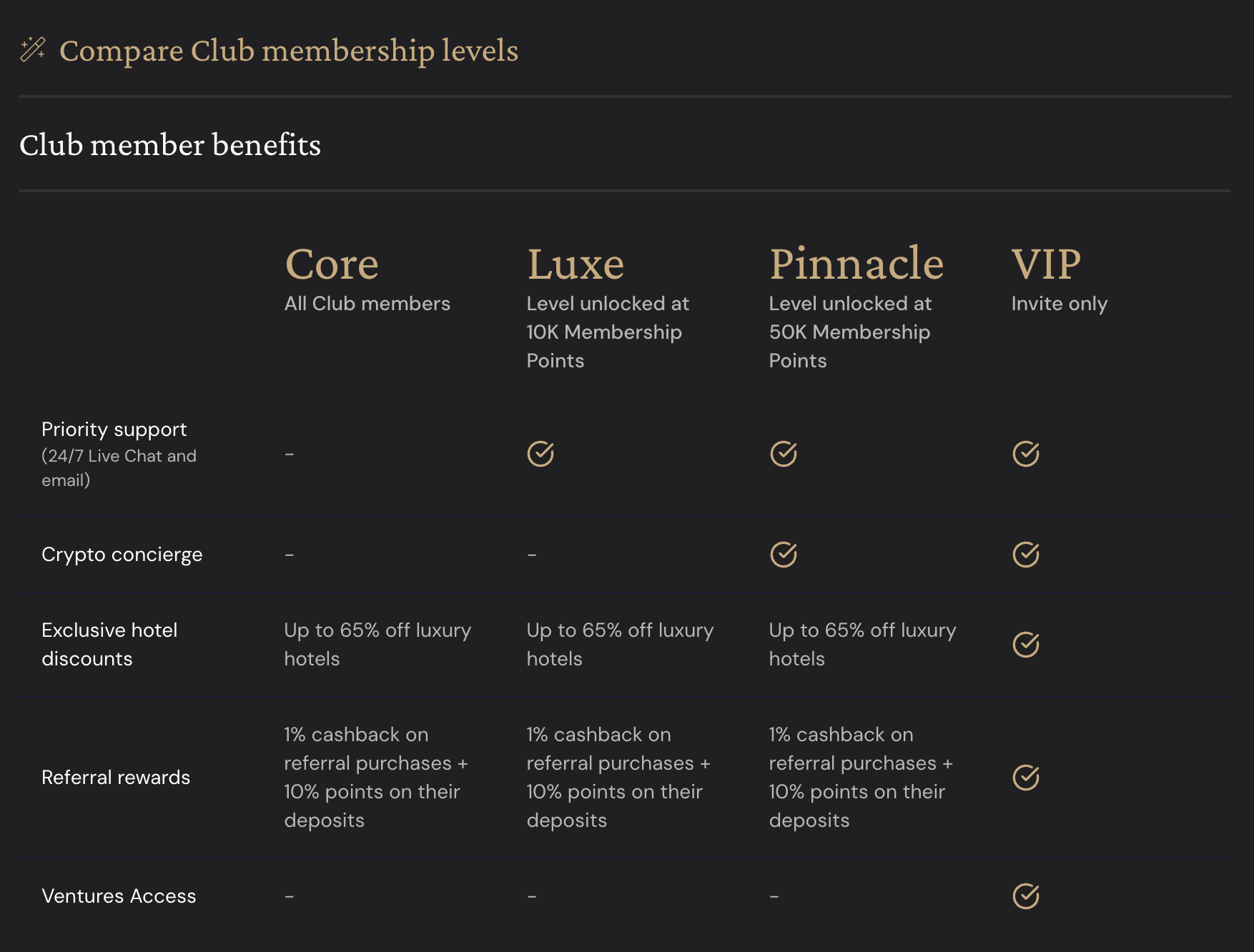

Membership tiers matter

EtherFi Cash is easier to understand if you separate the card from the membership layer.

The card gives you the payment rail. The club level changes some benefits, limits, and thresholds. That means two users can both have EtherFi Cash but get different practical value from it.

Membership level affects more than branding. It can change support, discounts, referrals, card benefits, and access.

The practical question is not “does the card say 3%?” It is:

- What tier am I in?

- What spend qualifies?

- What happens after the monthly threshold?

- Which benefits do I actually use?

The earn side is useful, but separate

EtherFi also shows an earn layer around liquid strategies and stable assets. This is part of the broader account story, but I would not mix it emotionally with card rewards.

Card cashback is one thing. Yield and vault strategies are another. Both can be useful, but they have different risks.

The earn layer is attractive, but it should be evaluated separately from the card’s cashback promise.

My rule: treat the card as a spending tool first. Treat yield products as separate financial products with their own risk assumptions.

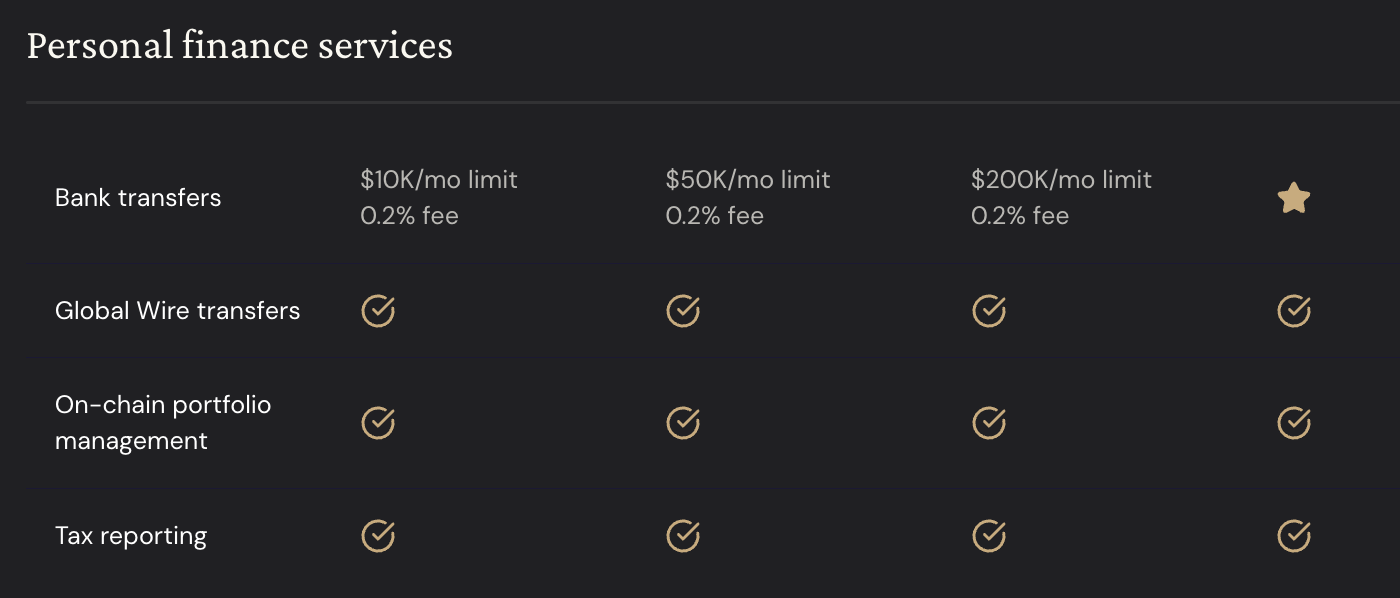

EtherFi Cash card fees, limits, and withdrawals

The card is more compelling if you actually use the broader account services: bank transfers, wires, portfolio management, tax reporting, and spending in USD/EUR. But fees and limits can change the real value quickly, especially if you plan to move money in and out often.

Limits and fees can matter more than cashback if you move larger amounts or use the account for travel/business spending.

Before relying on the card, check:

- Is the card available in your country?

- Which assets can be used or connected?

- What are the bank transfer and wire limits?

- Which fees apply to your currency and transaction type?

- Are ATM withdrawals or cash advances supported, and what do they cost?

- What happens if collateral value moves sharply?

- What repayment schedule applies to your account?

- Which purchases are excluded from cashback?

For withdrawals specifically, I would not assume they behave like normal merchant purchases. Check the current EtherFi docs and issuer terms before using the card for cash access.

My take

EtherFi Cash is one of the cleaner crypto card ideas right now because the card is not trying to be only a rewards gimmick. The interesting part is the link between real-world spending and a crypto-native account.

I would consider it if you already use EtherFi, already hold crypto, and want Apple Pay / Google Pay plus cashback without immediately selling assets. If that sounds like you, start with the referral signup link so any available extra cashback is attached before onboarding.

I would be more cautious if you only want simple cashback, do not want borrowing mechanics, or have not read the card terms for your region.

As always: read the latest terms, check availability in your jurisdiction, and do not borrow against volatile assets unless you understand the downside.